![]()

Rates of Change

Submitted by Atlas Indicators Investment Advisors on May 25th, 2026

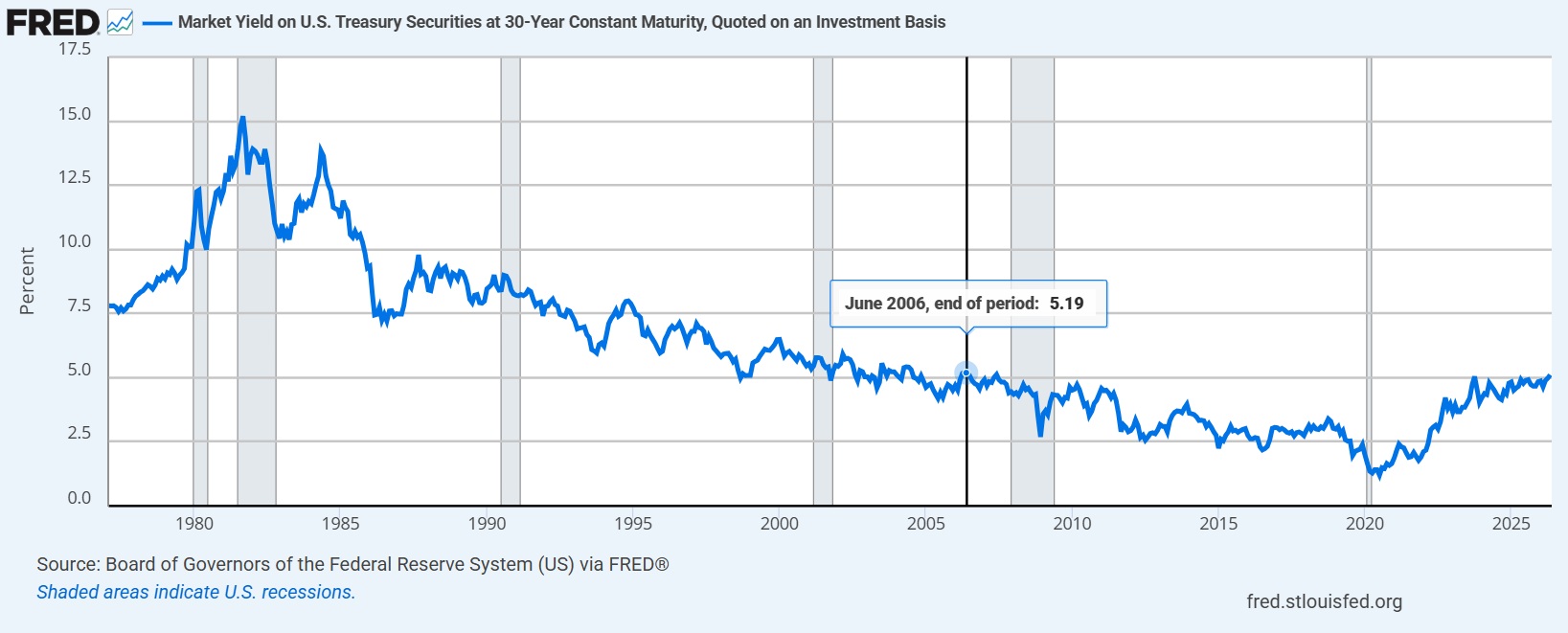

This was potentially a telling week for interest rates in America on the extreme ends of the yield curve. Way out on the right of the curve is the 30-year treasury bond. Its yield is what lenders to the American government can expect to be paid for the long-term loan. It reached 5.18% earlier this week, the highest level since 2006 (see chart above). That came on the heels of a rapid uptick to 5.00% on May 14th that pushed to 5.12% on May 15th. This is not just a crossing of an arbitrary threshold but could also be a sign of future borrowing costs across the American economy.

There were signals for the left-hand or short-term side of the yield curve as well this week. The Federal Open Market Committee (FOMC) released their most recent meeting minutes on Wednesday. This meeting was held April 28-29 and concluded with the FOMC leaving the overnight lending rate banks charge each other unchanged. It also, however, produced the highest level of dissent within the committee since October 1992 as four officials voted against the majority decision. Additionally, a majority of participants highlighted that “some policy firming would likely become appropriate if inflation were to continue to run persistently above 2.0%.” According the Fed’s preferred measure of inflation (the core PCE Price Index), the year-over-year change has not been under this target since February 2021.

Vulnerabilities always exist in markets and economies, but the Fed suggested that some of them are notable at this time. They believe that leverage in the financial markets has notable risks as hedge fund leverage remained high as did leverage at life insurance companies. By contrast, they were less concerned about exposures within the banking system.

Change could be coming for the yield curve driven by two forces. First, markets price long-dated treasury bonds as federal government’s borrowing costs are reaching territory not seen in nearly two decades. This could have knock-on effects for other borrowers across the economy which might accumulate quietly for a while and then suddenly be felt all at once. Simultaneously, policy makers are hinting at the potential need to push short-term rates higher, something which was unfathomable at the start of this year. This does not have to be awful news, however. The yield curve is not inverting, a condition which can often precede a recession. Instead, markets could be signaling that America’s economy remains strong enough to continue growing even as higher rates potentially loom on the horizon.