![]()

Put It on Their Tab

Submitted by Atlas Indicators Investment Advisors on April 29th, 2026

The Global Financial Crisis (GFC) of the aughts was fueled by creative financing. Firms competed feverishly to design loan products that made it easier for borrowers to qualify, often abandoning the prudent standards that had long shaped America’s mortgage market. It ended badly.

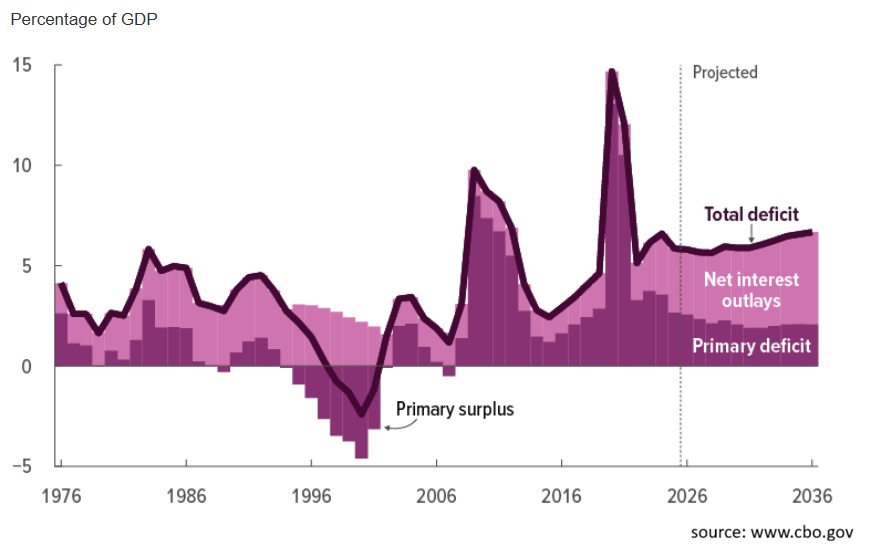

Today, concerns are growing about a far less creative form of financing: America’s expanding debt and deficit. Historically, this sort of lending has been about as boring as it gets. Folks and institutions lend to the United States because it has long been the safest borrower in the world. Especially in the aftermath of the GFC, Uncle Sam’s safety was sought after. On the other side of the transaction, the federal government has been willing to spend at an unparalleled pace. The result is starting to resemble something akin to a balloon payment-mortgage. America has been borrowing at relatively low rates and has been able to service the interest comfortably, but interest costs are now rising and expected to accelerate, a trend Atlas has highlighted several years in our notes on the federal budget.

According to the Congressional Budget Office (CBO), net interest payments are likely to be the fastest-growing line item in the federal budget. They project it will double in the next 10 years, moving from $1.0 trillion this year to $2.1 trillion by 2036. More troubling, interest payment growth is now expected to outpace that of the economy starting in five years and for the foreseeable future thereafter. For all of the past 15 years and most of the past 60 years, economic growth has exceeded interest payment growth, a dynamic that has helped make lending to the U.S. so attractive (i.e., safe).

Faster economic growth seems like a reasonable solution, but America has challenges. Demographics, which were a tailwind for decades, are morphing into a headwind. Slower labor force growth means our economy will be more dependent on productivity gains to drive economic expansion. Demographics are predictable (just look at the birth rate from 18 years ago and you know virtually how many new adults the nation will gain). They also move glacially. Productivity enhancing technology is less predictable although more exciting. Such gains may arrive, but counting on them to outpace rising interest rates might be risky. If economic growth fails to accelerate meaningfully, today’s comfy borrowing profile could evolve into a balloon payment. At some point the tab comes due, and the longer it remains open, the more difficult it will be to settle.