![]()

April 2018 Employment Situation

Submitted by Atlas Indicators Investment Advisors on May 11th, 2018

Firms continued adding to their payrolls as the second quarter of 2018 got underway. According to the Bureau of Labor Statistics, 164,000 net new jobs were created in April. Additionally, March’s tally was revised upward to 135,000 (originally just 103,000). Headlines focused on the unemployment rate because it dropped below 4.0 percent for the first time since December 2000, reaching 3.9 percent.

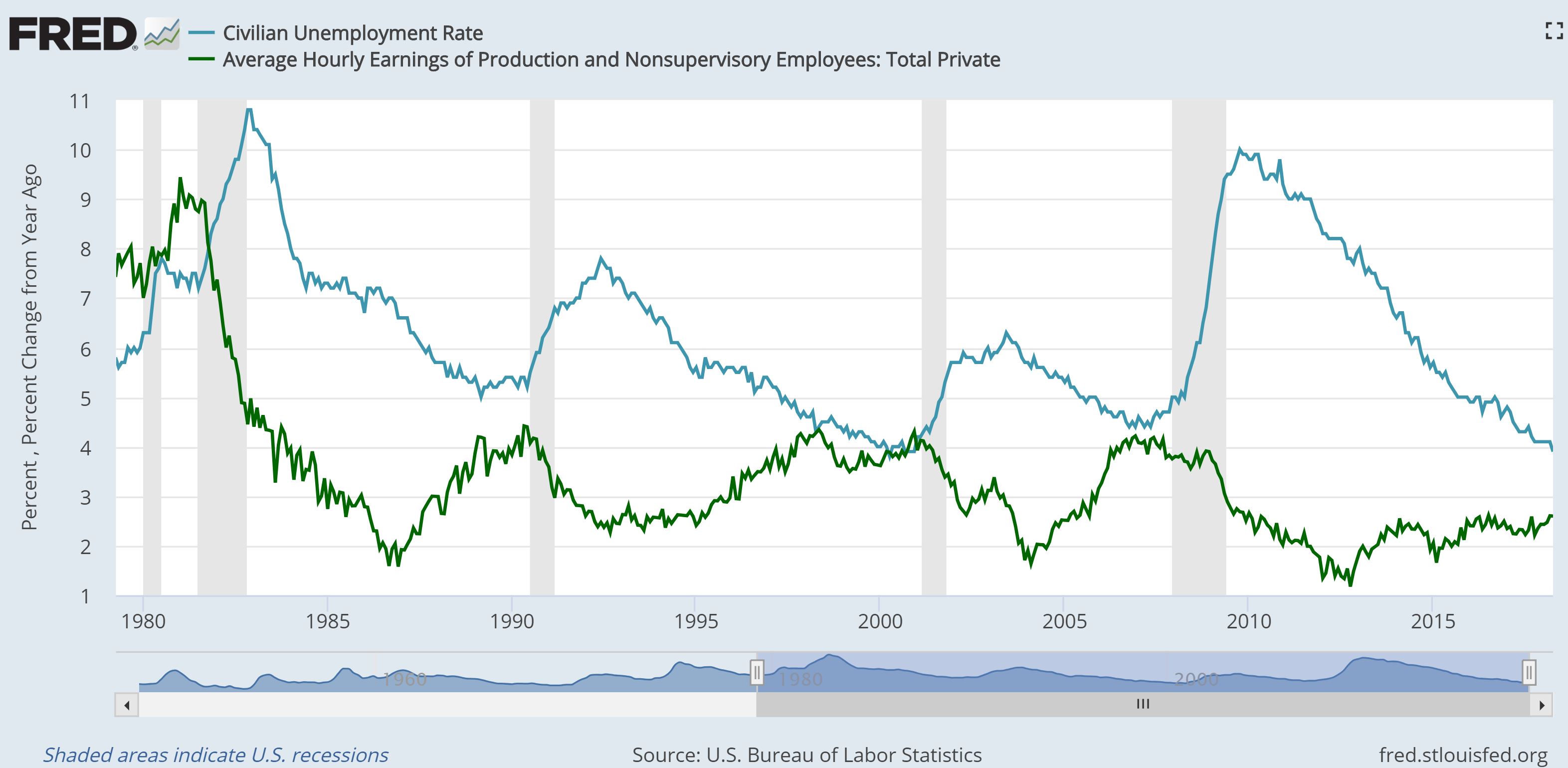

Notwithstanding the low jobless rate, employers haven’t been compelled to offer much in the way of higher wages. Average hourly earnings barely budged, rising 0.1 percent in April and growing just 2.6 percent versus a year ago. Additionally, these two tallies were downwardly revised for March. This is one of the puzzling relationships of the current expansion. In Friday’s note, J R mentioned the Philip’s Curve; in short, the curve expresses an inverse relationship between the unemployment rate and wage growth, but it is not acting as potently in this business cycle as theory predicts. As you can see above, the hourly wages of production and nonsupervisory employees (green line) is not growing as quickly as in prior expansions, especially in light of the rapidly declining unemployment rate (blue line).

Partly due to the mystery of wage growth, America’s employment situation looks a bit Goldilocks right now. Firms are willing to add to their payrolls. This puts money into the pockets of consumers. Since domestic consumption accounts for nearly 70 percent of American output, this should help push the economy further along. Meanwhile, firms are not compelled to make accelerating wage concessions for some reason (it could be the one we mentioned here), so companies are not forced to pass on faster labor cost to end consumers. Of course, in Robert Southey’s tale, the fun ends when the bears come home. This Goldilocks period won’t be here forever, so Atlas won’t be napping no matter how comforting things seem.