![]()

March 2018 Institute for Supply Management

Submitted by Atlas Indicators Investment Advisors on April 13th, 2018

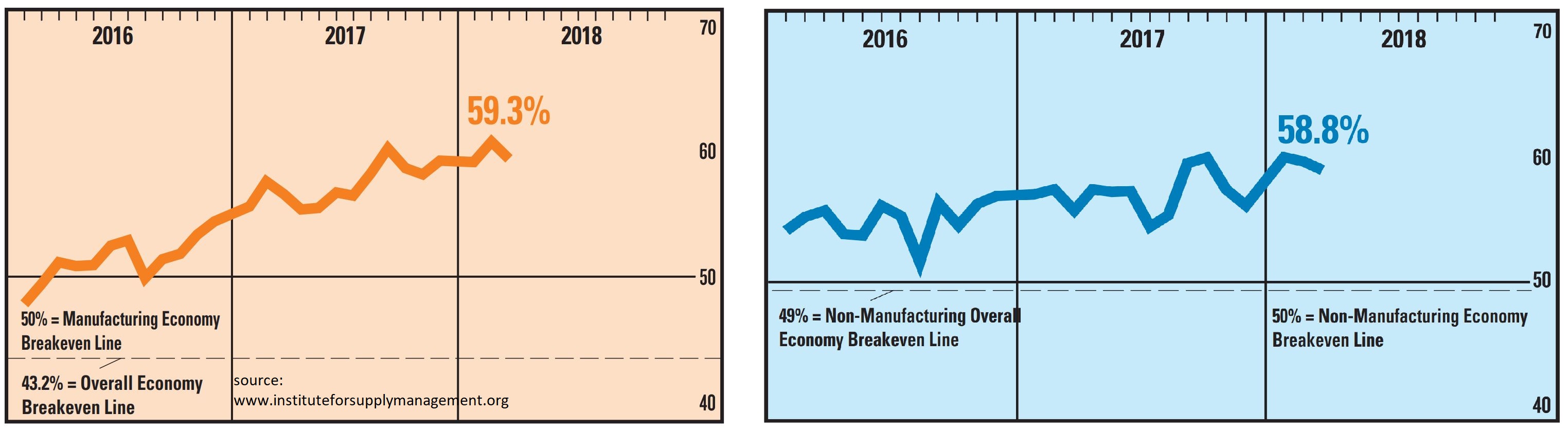

Economic output remained strong on both sides of the economy according to the Institute for Supply Management. At 58.8, their reading for the services portion of the economy remained well ahead of 50.0 which is associated with no change. Likewise, the manufacturing index was 59.3. Admittedly, both measures fell marginally, but they did so from lofty levels and are still very strong.

Nonmanufacturing showed strength in both leading and coincident components. New orders remained elevated at 59.5, down just 0.5 from a month earlier. These should become actual output in the months ahead, boding well for gross domestic product (GDP). Employment continues looking positive as it rose 1.6 to 56.6 which is high for this component. Supplier deliveries added to the positive tone of the release; they are lengthening which could result in additional hiring or even capital outlays.

Manufacturing fell but did so from a 14-year high. New orders and export orders were strong on this side of the economy as well, also boding well for future GDP. Deliveries’ reading were elevated, which might also lead to added hiring or equipment investment. Some issues with inflation could be on the horizon for this segment of the economy as the reading for input costs rose to an eight-year high.

Atlas watches these indicators for a few reasons. First, these indicators cover both sides of the economy. Secondly, they are released soon after the month in which the data are collected ends, so they are timely. Finally, they are recorded every month, unlike some indicators which aggregate quarterly information. Despite these features, it is important to remember that they are surveys, making them dependent on the feelings of the managers answering questions and do not include hard data. Nevertheless, they often represent the general direction of the economy and are currently pointing to continued expansion.